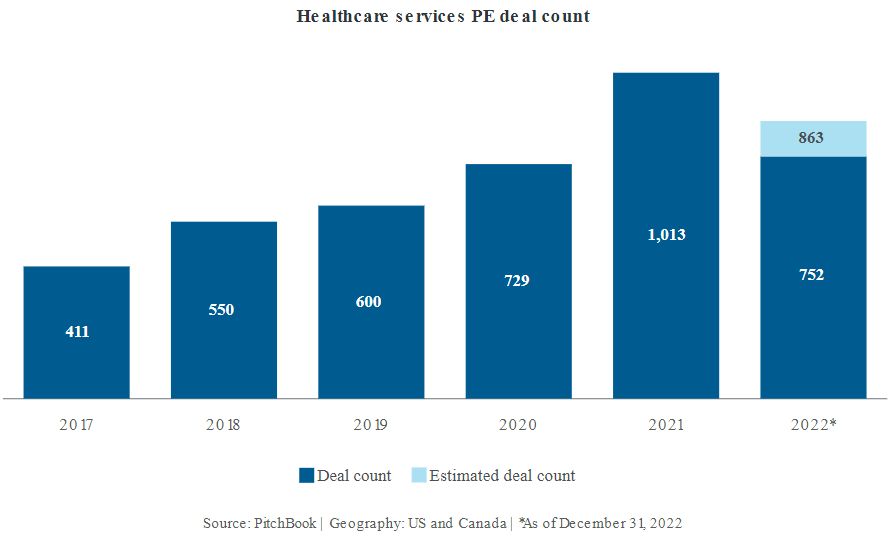

After being squeezed out of the R&W insurance market in 2021, deals in the healthcare services sector have regained interest from insurers and are seeing lower rates and greater competition. Healthcare has been a bright spot for deal activity over the past year (see chart). As the number of private deals involving healthcare services rose, demand for representations and warranties (R&W) insurance in the space also increased. Despite turning away from this sector in 2021, insurers are more motivated to provide R&W insurance coverage for healthcare transactions in the current environment, particularly since deal activity in other sectors has moderated.

Indeed, more insurers are competing to underwrite a wide range of healthcare services and life sciences deals, including those involving home health services, behavioral health centers, physician practices, providers of electronic medical record solutions, and contract research organizations. These factors have contributed to an overall reduction in rates, consistent with the R&W insurance marketplace generally, and have also left buyers better positioned to negotiate policy terms.

Why has the landscape changed for R&W insurance in healthcare? How has this affected terms? And what are the limitations of the current market?

More Market Participants

Even among regulated industries, R&W underwriters have historically considered the healthcare industry to be challenging, given the complexity of healthcare laws and regulations and the lack of audited financial statements for many privately held healthcare targets. In the past ten years, the appetite of R&W insurance carriers to underwrite healthcare deals has waxed and waned.

When R&W insurance first became available for healthcare deals from one insurer, obtaining coverage (especially if the target received government reimbursement) involved significant time, expense, and uncertainty as to whether insurance would ultimately be available. Coverage (if available) was subject to a higher retention for breaches of healthcare representations than non-healthcare representations. The market opened up several years ago, with more insurers offering R&W insurance for healthcare deals using more or less the same underwriting processes, fees, and terms used in other sectors.

Progress stalled for a time, with some insurers pulling back based on claims experience or business focus. Few insurers were interested in healthcare deals in 2021, when deal activity soared across sectors. At that time, it was not uncommon for brokers to receive only one or two — or no — quotes for healthcare deals, leaving little leverage to negotiate terms. The terms became more expensive and heavily qualified with exclusions, to a point where some sellers and buyers found R&W insurance to be an ineffective risk-shifting tool and were forced to revert to a non-insurance deal with more fulsome contractual indemnity.

In 2022, some R&W insurers began to buck the trend, however, making a conscious decision to learn about the sector and gain market share. Private equity deals in healthcare remained robust even as deal activity declined in most other sectors, making the sector hard to ignore. At the same time, the number of R&W insurance providers kept increasing. More than 25 providers now offer R&W insurance. In this environment, more carriers began bidding widely, including on healthcare services transactions that they may have stayed away from in recent years.

Lower Rates, Better Terms

Increasing competition has benefited buyers, giving them more negotiating power to secure the coverage they need to manage risk effectively.

Although premiums increased sharply in 2021, reaching 6% – 8% or more of the policy limit for some healthcare deals, they dropped steadily in 2022 and now hover around 3% to 3.5% of the policy limit. This is consistent with pre-pandemic levels and close to premiums in other sectors.

With greater competition, buyers are now better able to negotiate policy terms in a number of areas, including price, retention, and the duration of healthcare representations. Buyers have better success at keeping insurers’ limitations on the wording of the insured representations to a minimum. Additionally, given that buyers are seeing quotes from carriers they have not worked with before, they are seeking more input from brokers and advisers on factors beyond terms within quotes, such as underwriting style and claims experience.

Another noteworthy development is a technical improvement in coverage. In recent years, it has become common for R&W insurers to argue that certain types of claims should be covered by another insurance (such as cyber insurance or professional liability insurance) for the target, even if there were breaches of representations that should trigger coverage under R&W insurance. Such “excess, no broader than” restrictions required that other insurance to be exhausted first and gave the R&W insurer a chance to say that its coverage obligation was not triggered if a particular type of loss was not within the scope of the other insurance. This was unpopular among buyers and their advisers for years, and its usage has now become infrequent. As a result, buyers can be more confident that the coverage trigger for their R&W insurance is determined by the wording of the representations and not dependent on the coverage position of another insurance policy.

Limitations of the Current Market

Insurers still take extra precautions in providing R&W insurance to healthcare services companies. They continue to make individual determinations on whether to quote or decline a particular deal and whether to propose exclusions based on the nature of the business, relationships with the buyer and advisers, and characteristics of the transaction.

Like buyers, insurers pay close attention to regulatory changes and adjustments to compensation models that could increase government scrutiny, cause more disputes with payers, or in other ways increase the risk of significant losses.

Moreover, the number of insurers that underwrite a wide range of healthcare businesses is still limited. Some carriers cover only audited or healthcare-adjacent businesses like healthcare IT. Some participate in the healthcare sector only occasionally — and may exclude billing and coding risks when the insured company receives a significant level of government reimbursement.

Companies that are able to provide services to patients without strict licensure requirements (e.g., home health services) or that may provide services directly to patients in a residential setting have traditionally received more scrutiny than other businesses. This can lead to declinations or up-front policy exclusions for certain industry-specific risks.

In the current environment, however, R&W insurance is more widely available even in cases where the kinds of risks discussed above are relevant. But some insurers may change direction if the market for healthcare transactions changes course, or if overall deal flow again reaches peak levels and insurers have the option to meet their earning targets by underwriting deals in industries that are deemed less risky or complex.

* * *

Although the number of individuals who specialize in underwriting healthcare services deals is limited, a growing number of underwriters, underwriting counsel, and brokers have gained expertise in recent years and have become more comfortable participating in the sector. With new players having entered the market since the beginning of the pandemic, and insurers staffing up after experiencing bandwidth issues in 2021, buyers are likely to continue to have more options for obtaining R&W insurance than they have had in the recent past. Given this changed reality, it is important for buyers to look beyond the terms on paper and to work with their advisers in selecting an underwriter and determining what is negotiable.